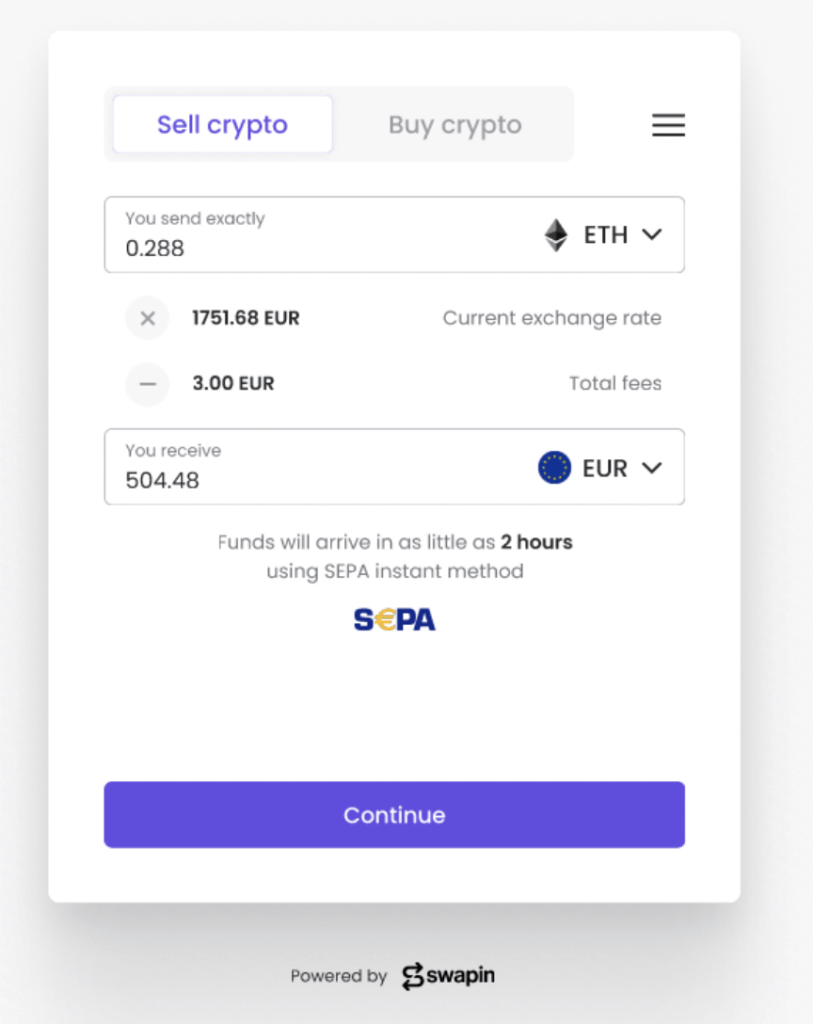

What is a crypto to fiat payment gateway and how does it work

Despite a growing demand for crypto payments, accepting crypto often raises practical questions around pricing volatility, settlement timing, and how the funds ultimately land in your bank account. For businesses operating in traditional fiat currencies, holding crypto introduces unnecessary complexity that can derail your cash flow management.

A crypto to fiat payment gateway addresses this exact gap. It allows businesses to accept cryptocurrency payments while receiving funds in fiat (USD, EUR, GBP etc.) removing exposure to price swings and keeping your operations streamlined.

Below, we’ll explain what a crypto to fiat payment gateway is, how the conversion process works, and why thousands of businesses choose this model over holding crypto directly.

A crypto to fiat payment gateway is a payment solution that accepts cryptocurrency from customers and automatically converts it into traditional currency for your business.

From the customer’s perspective, the payment happens in Bitcoin, Ethereum, or stablecoins. From the businesses’ perspective, the payout lands in dollars or euros, directly to the bank account.

Unlike basic crypto payment processors that stop at acceptance, crypto to fiat gateways focus on real-time conversion and settlement. The idea is for merchants to accept digital currency without requiring them to manage wallets, monitor exchange rates, or navigate price fluctuations.

How crypto to fiat settlement solves crypto management issue

Price movements can affect the final value of a payment between the time it’s received and when you convert it. For businesses that price products in fiat, this makes revenue harder to predict and manage.

There are also operational considerations.

Your pricing needs to stay consistent, refunds should be straightforward, and financial reporting should follow familiar processes. Holding crypto complicates each of these areas and requires new accounting protocols.

Fiat settlement removes these friction points entirely. Crypto payments get converted automatically at market rates, allowing you to receive funds in stable currency while still offering cryptocurrency as a payment option to tech-savvy customers.

How a crypto to fiat payment gateway works

A crypto to fiat payment gateway follows a simple payment flow from initial payment to fiat settlement.

The customer selects cryptocurrency as the payment method at checkout

The payment gateway generates the required payment details and waits for the transaction to be confirmed on the blockchain

Once confirmed, the received crypto is automatically converted into fiat currency based on the agreed conversion terms

The converted fiat amount is settled to the business through standard payout methods, such as a bank transfer

From the business’s side, the payment is received in fiat and can be processed like any other incoming payment

This setup allows customers to pay in crypto while businesses receive funds in a stable currency without handling crypto directly.

When should businesses choose crypto to fiat payment gateway

Businesses viewed crypto payments as an all-or-nothing solution that needs to be built from the ground up.

That’s not the case anymore. Crypto to fiat payment gateways allow businesses to tap into the $2.4 trillion crypto payment market without overhauling their entire financial infrastructure.

This approach has gained serious traction when customers are pushing to pay in crypto, but businesses want to keep their pricing, accounting, and payouts flowing in familiar fiat currencies. It’s become the go-to solution for companies handling cross-border transactions, high-ticket purchases, or one-time deals where speed trumps everything else and certainty matters more than speculation.

For businesses that see crypto as an additional payment method, crypto to fiat gateways have opened a surprisingly straightforward path forward.

What to look for in a crypto to fiat payment gateway

In practice, the differences between providers are defined by conversion reliability, automated settlement, and fiat currency coverage. Settlement speed has become a make-or-break factor, particularly for businesses that live and die by predictable cash flow rhythms.

Conversion should be automatic and predictable

Look for a provider that converts crypto to fiat without manual steps or timing decisions. Automatic conversion reduces exposure to price changes and keeps payments simple to manage.

Settlement should fit existing payout workflows

The provider should support direct fiat payouts through familiar methods, such as bank transfers, and offer settlement speeds that match how the business already operates.

Supported currencies should match customer and business needs

Check which cryptocurrencies customers can pay with and which fiat currencies the business can receive. Limited currency support can create friction later.

Reporting should be clear and easy to reconcile

Payment records, conversion details, and settlement reports should be easy to access and understand. This helps payments fit into existing reporting and reconciliation processes.

Compliance and geographic coverage should be clear upfront

The provider should clearly state where it operates and how compliance is handled, so there are no surprises when expanding into new markets.

The process for off ramping (selling) crypto includes the following steps:

Payment initiation

The customer first enters the amount of crypto they want to sell, selects the cryptocurrency and payout currency, and provides their bank account details for the fiat transfer.

Email confirmation

A confirmation email is then sent to the provided address containing a 6-digit verification code, which the customer uses to confirm the request.

Verification process

After confirming their email, the customer proceeds to a one time identity verification that can take up to a couple of hours.

Crypto transfer

Once verification is complete, the customer continues with the transaction. A dedicated wallet address is generated for the order. The customer sends the crypto to this address either by copying it into their wallet application or by scanning the provided QR code.

Payment order and settlement

After the crypto is received, it is automatically converted into fiat and a payment order is initiated to the customer’s bank account. If the receiving bank supports instant SEPA transfers, the payout can be completed within minutes.

Swapin crypto to fiat payment gateway

Common misconceptions about crypto to fiat payments

A common misconception is that accepting crypto automatically means you’re stuck holding crypto. In reality, the best gateways convert payments instantly, so businesses never actually touch digital assets, they just get the benefits of crypto-paying customers.

Another assumption is that crypto to fiat payments turn into a management nightmare. For most businesses, the experience feels remarkably similar to other digital payment methods, with the bonus of unlocking an entirely new customer segment that prefers paying in crypto.

There’s also this stubborn belief that only crypto-native companies use these solutions. In practice, traditional businesses across industries are plugging in crypto to fiat gateways simply as another way to get paid, treating it like adding PayPal or Apple Pay to their checkout flow.

Crypto to fiat payment gateways vs holding crypto directly

Holding crypto directly gives businesses complete control over managing assets, but it also means managing volatility and operational complexity head on.

Crypto to fiat payment gateways such as Swapin remove volatility and reconciliation issues entirely. They prioritise operational simplicity by converting payments the moment they hit and settling everything in fiat currencies, shielding businesses from market dips and keeping revenue streams predictable and manageable.

Is a crypto to fiat payment gateway right for your business?

A crypto to fiat payment gateway has become the practical choice for businesses wanting to reach crypto-paying customers. If you plan to receive funds primarily in fiat, value predictable payouts above everything else, and want to dodge the complexity of managing crypto directly, this model is likely hitting all the right notes for your situation.

For businesses expanding into crypto payments for the first time, a crypto to fiat gateway delivers the smoothest onramp and offramp possible while keeping operations controlled and running exactly like they always have.

An all-in-one crypto to fiat payment gateway solution

Crypto to fiat payment gateway solutions are a viable and practical solution for modern businesses. As merchants explore payment solutions that fit business needs while also ensuring customer satisfaction, Swapin’s crypto payment gateway solution offers flexibility that doesn’t compromise on security.

The state of B2B crypto payments in Europe: insights from Swapin’s CEO

This article draws on a recent Founders Unchained conversation with our CEO, Evald-Hannes Kree, on building Swapin, the crypto payment infrastructure for regulated businesses. The discussion explored how trust, compliance, and operational discipline have become central to adoption in Europe.

Founders Unchained, hosted by entrepreneur Darius Kraucionis, features candid conversations with founders about the realities of building companies from the ground up. The insights below expand on that discussion, focusing on how regulation and infrastructure are shaping crypto payments for businesses today.

For nearly a decade, cryptocurrencies promised to reshape global payments. Adoption among established retail, luxury, aviation, and automobile businesses, however, remained limited. The primary constraint was not transaction speed or cost efficiency. It was the absence of trust at an infrastructure level.

Early crypto payment systems lacked the operational maturity required by serious businesses. Regulatory frameworks were inconsistent, banking relationships were fragile, and payment rails were not designed to meet the compliance, auditability, and reputational standards expected by established merchants.

The limitation was practical rather than ideological. Businesses could acquire crypto, but using it reliably in real commercial contexts remained difficult.

As Evald-Hannes puts it:

“Owning crypto was possible, but using it in real life was not. That gap was obvious from the beginning.”

Swapin was founded to address this structural gap by focusing on the crypto payment infrastructure rather than speculative use cases.

From early experiments to a regulated business model

Swapin began taking shape between 2015 and 2016, during the first major wave of crypto adoption. At the time, industry attention was concentrated on exchanges and asset trading. Practical commercial usage received far less attention.

Before the company was formally established in 2018, the founding team spent nearly two years building backend infrastructure for an early mobile wallet project in Estonia. This pilot phase exposed both the technical constraints of early crypto systems and the lack of clear regulatory guidance.

Clearer legislation introduced in Estonia in 2018 created the conditions required to formalise the business. Operating within defined legal boundaries was not treated as a constraint, but as a prerequisite for long-term viability.

Reflecting on that period, Hannes says:

“It was extremely difficult to build a crypto payments business at that time. The technology was early, and there was no real legal framework. Once regulation started to take shape, it became possible to build a real company.”

Regulation and long-term operating certainty

Regulation is often framed as a barrier to innovation in crypto. For enterprise adoption, the opposite tends to be true. Businesses do not avoid regulation; they avoid uncertainty.

Over the years, Swapin has operated through repeated regulatory revisions, banking exits, and licensing changes across Europe. Each shift required adaptation at both technical and organisational levels. The experience reinforced a consistent lesson: stable operating conditions matter more than permissive ones.

Today, Swapin operates within major European banking infrastructures and focuses on compliance-driven crypto processing, including stablecoin-based and cross-border payment flows. Regulation is treated as a permanent operating condition rather than a temporary hurdle.

“Laws changed repeatedly, banking partners came and went, and we had to adjust continuously. That pressure is real, but it is also what forces operational discipline.”

The shift toward B2B crypto payments

During periods of rapid crypto market expansion, much of the industry pursued retail adoption at scale. Customer acquisition costs increased, competition intensified, and profitability was often deprioritised in favour of growth metrics.

Swapin tested this approach following a fundraising round, expanding its retail focus during a market downturn. The economics proved inefficient, particularly in an environment dominated by large, well-capitalised competitors.

A strategic shift followed. The company redirected its efforts toward B2B clients, where decision-making is driven by reliability, service quality, integration depth, and regulatory clarity rather than by incentives or brand visibility.

“In B2B, success depends on direct relationships, service quality, and how well the infrastructure integrates. Those factors matter far more than scale alone.”

Over the past two years, Swapin has concentrated on supporting businesses for whom crypto payments must operate efficiently and in full compliance with existing financial systems.

Size, flexibility, and payments infrastructure risk

Scale can provide advantages in payments infrastructure, but it also introduces rigidity. For businesses operating in evolving regulatory and technological environments, adaptability becomes a meaningful risk factor.

Swapin supports clients across sectors including financial services, real estate, and private aviation. Serving these industries requires custom integrations, rapid decision-making, and close operational collaboration.

Smaller, focused teams are often able to respond to regulatory or infrastructure changes faster than large institutions constrained by layered approval processes.

Hannes notes:

“Flexibility allows us to adjust quickly as the market changes. In payments infrastructure, that responsiveness directly affects reliability.”

What this means for businesses considering crypto payments today

Crypto payments have reached a more mature phase. The conversation has moved away from speculation and toward infrastructure, compliance, and operational resilience.

For retail and luxury businesses evaluating crypto payments today, the most important questions are practical rather than technical:

Can this integrate cleanly with existing payment and accounting systems?

Does the provider operate within clear European regulatory frameworks?

Are banking relationships stable and durable?

Will the infrastructure remain reliable over multiple market cycles?

Crypto payments today are increasingly associated with operational readiness rather than early adoption. Businesses that approach the space through the lens of infrastructure, regulation, and long-term stability are better positioned to extract real value.

Swapin’s trajectory reflects a broader industry shift. Sustainable adoption occurs when technological capability is aligned with regulatory discipline and operational maturity.

Interested in knowing more about how to integrate crypto payments? Learn more about how Swapin can help power your business transactions or get started today.

Open banking vs crypto: what’s best for high-ticket businesses?

Customer expectations are shifting toward global accessibility. And the payment solutions matter more than ever, especially in industries where values are high, clients are international, and timing determines whether revenue is realised or lost.

Two payment methods are shaping this landscape: open banking payments and crypto payment rails. Both promise faster, more efficient financial movement than legacy card networks or traditional bank transfers, yet they operate in fundamentally different ways.

The choice of payment method affects settlement speed, risk exposure, customer experience, geographic reach, and ultimately the business’s ability to close transactions when it counts.

In this guide, we dive deeper into both solutions and see which one comes on top.

At its core, open banking is a regulatory and technological framework that allows customers to authorize third parties to securely access their financial data or initiate payments directly from their bank account. Instead of scraping interfaces or relying on manual transfers, these interactions happen through structured APIs exposed by banks.

Open banking does not eliminate bank processing times, compliance checks, or clearing schedules. It does, however, facilitate access and initiation, but the actual movement of money still follows the established domestic rails, SEPA, Faster Payments, ACH, and their equivalents.

Open banking can be efficient, but it doesn’t fundamentally change how banks move money across borders or during high-value, time-sensitive moments.

How does open banking payments work in practice

Open banking payment is a straightforward process for the customer. They choose “pay by bank,” authenticate through their banking app, and authorize a transfer.

The authorization triggers a bank-to-bank payment through the appropriate domestic rail, SEPA Instant in parts of Europe, Faster Payments in the UK, ACH in the United States, and so on.

Settlement times depend heavily on the underlying bank rail, the region, the time of day, and compliance rules. Some banks support instant transfers, while others process transactions in batches. Funds can take anywhere between a few minutes to days to settle.

For businesses, open banking improves user experience and reduces card fees, but it doesn’t fully remove the variability inherent in bank-led settlement.

Payment reliability still depends on the customer’s bank, the corridor, and the domestic payment network. High-value or cross-border transactions may still face delays, manual reviews, or reconciliation challenges, issues that become more acute when urgency is part of the transaction.

Benefits of open banking for businesses

Open banking has been a game changer for most businesses, primarily for these 3 reasons:

One, open banking reduces reliance on card networks, allowing businesses lower transaction fees and avoid chargebacks.

Payments initiated directly from a bank account are also authenticated using the customer’s own banking credentials, reducing fraud exposure and disputed transactions.

Two, open banking streamlines the checkout experience allowing them to complete payments through their banking app. This is particularly helpful for domestic, mid-value transactions where speed and convenience are more important than global reach.

Three, businesses receive structured payer data, which enhances reconciliation and reduces manual intervention. For subscription or recurring revenue models, open banking–powered account verification reduces failed payments and onboarding friction.

For many businesses, these benefits are significant, but they apply most strongly in markets with mature open banking ecosystems and primarily domestic customer bases.

The limitations of open banking

Because open banking depends on domestic bank rails, its reliability and speed vary widely by region and institution. Some banks support near-instant transfers while others still rely on batch processing cycles.

In cross-border scenarios, open banking rarely accelerates settlement, the transfer still moves through correspondent banking networks, with all the associated delays and uncertainties.

Europe’s PSD2 accelerated adoption, but implementation differs across banks and markets. The UK has a strong, unified standard but other regions don’t. In the United States, open banking adoption is largely voluntary, leading to uneven API quality and inconsistent support for payment initiation.

These gaps create practical challenges for businesses. High-value payments may trigger security reviews regardless of initiation method. Transfers can still be held, delayed, or declined by the sending bank. International buyers may experience unpredictable processing times or FX discrepancies. And while open banking removes layers of friction compared to cards, it does not remove the dependency on banking hours, clearing times, or domestic constraints.

For businesses operating across borders or handling urgent, high-ticket transactions, these limitations become material and often costly.

What are crypto payment rails

Crypto payment rails are built on blockchain technology that allow value to move globally, at high speed, without relying on traditional banking intermediaries. Where open banking connects directly to bank accounts, crypto rails operate outside of the banking system entirely, transferring digital assets, most commonly stablecoins, pegged to traditional currencies.

Crypto payment rails function as an independent settlement network, where payments are executed in minutes, not processed through a chain of banks. There are no cut-off times, no regional restrictions, and no reliance on domestic clearing systems.

More importantly, the majority of enterprise payments use stablecoins, which behave like digital representations of the US dollar or euro. That means value is stable, predictable, and compatible with traditional treasury workflows once converted back into fiat.

How crypto payment rails work

A client sends a stablecoin payment to a business’s receiving address and the payment arrives within minutes. Businesses can either hold the digital asset or automatically convert it into fiat currency.

There is no dependency on banking hours, compliance queues, or clearing schedules. Payments settle 24/7 with a high degree of finality and traceability. Each transaction is recorded on-chain, creating a transparent audit trail that finance teams can reconcile without relying on intermediary statements.

The same workflow applies whether a buyer is in Dubai purchasing property in Portugal, or a client in Singapore booking a private jet departing from Nice. Crypto rails deliver a consistent experience globally and that’s something traditional rails struggle to replicate.

This operational predictability is one of the biggest reasons high-value industries are beginning to integrate crypto rails alongside their existing payment infrastructure.

Crypto payment rails address several of the pain points that businesses regularly encounter when handling large, urgent, or international payments.

Here are the top benefits of moving money with a crypto payment rail:

One, crypto transactions settle in minutes and require no involvement from intermediaries who can delay or block transfers. For time-sensitive sectors such as real estate reservation fees, last-minute aviation bookings, luxury goods customers who expect immediacy, this reliability directly affects revenue.

Two, crypto rails offer global accessibility. Whether the sender is in New York or Nairobi, the settlement process works the same. There are no corridor-specific delays or restrictions, and no multi-bank routing that introduces uncertainty. High-value payments arrive in full, without intermediary deductions or FX erosion.

Three, crypto payments are available 24×7. Traditional bank transfers don’t settle on weekends, holidays, and outside business hours. Crypto rails operate continuously, which is critical for international clients who transact across time zones or for industries where opportunities arise outside the rhythm of banking hours.

Four, with crypto payments merchants receive the exact amount without hidden fees or unexpected deductions, every time. For businesses managing large payments where reconciliation accuracy matters, that predictability is a significant operational benefit.

Open banking vs crypto rails: what works best for businesses?

For global businesses, it makes sense to offer both payment options to provide clients flexibility.

Open banking works well for domestic, everyday, mid-value transactions where cost efficiency and streamlined authentication matter.

Crypto payment rails become essential when payments are cross-border, time-sensitive, high-value, or operationally critical. In these situations, the structural limitations of banking rails become business risks. Crypto rails offer global reach, speed, and settlement certainty that traditional rails cannot match.

For example, an internationalboutique yachting company can offer open banking for routine operations for local sales and bookings while offering crypto rails to high-ticket clients looking to move money quickly, from anywhere, at any given time.

Why high-ticket industries are adding crypto rails

Businesses operating in high-ticket industries such as real estate, private aviation, luxury retail, and automotive, are choosing to offer payment solutions that meet client needs best. Crypto payment rails are entering the picture not to replace open banking or traditional bank transfers, but to fill the structural gaps those systems cannot address.

Open banking improves the domestic experience, but it still relies on banking hours, domestic clearing systems, and regional compliance differences. Crypto rails solve the parts of the flow where businesses cannot afford uncertainty, global reach, settlement finality, and after-hours availability.

Accept crypto payments with zero integration and setup fees

Businesses assume accepting crypto payment means developing the infrastructure from scratch. And this couldn’t be farther from the truth.

Crypto payment links serve as the easiest entry point for businesses venturing into the crypto ecosystem. The clients simply click on the payment link, choose their preferred crypto currency to make the payment with, and complete the transaction. Meanwhile, the payment processor, in this case Swapin, receives the crypto payment and automatically converts it to fiat to the business’ bank account.

Thus removing volatility and allowing businesses to receive the exact invoiced amount in EUR, USD, or GBP. Reconciliation becomes just as straightforward, with each payment tied to an invoice or client reference, and the operational process around accounting remains unchanged.

Why high-ticket industries are adopting crypto payment rails

High-ticket industries benefit from instant settlements and crypto payment rails have enabled businesses to tap into a global client-base.

Across luxury real estate, private aviation, and high-end automotive, businesses are observing the same behavioural shift. Clients want faster and safer payment options. And with that, accepting crypto payments, particularly stablecoins, has become a popular way to remove last-minute blockages that typically slow or derail high-value transactions.

The biggest blockage high-ticket clients face is working around banking limitations. Businesses today operate across borders, hold funds in multiple currencies or digital assets, or scale businesses in markets where bank transfers are slow and compliance-heavy. Traditional payment rails often get in the way making transfers bounce, arrive late, or get held for verification.

When a client has a €200K closing payment to send, or a €60K car deposit to secure, they expect the payment process to match the premium nature of the purchase.

Where traditional payment solutions miss out

Bank transfers initiated after business hours don’t get processed until the next working day. Wire transfers route through multiple banks and intermediaries, adding on the FX fees and delays. It’s the same case with card payments as well.

Multiple intermediaries slowing down the payment processing. And while debit cards are generally accepted worldwide, there are still geographical constraints where each country has its own banking regulations affecting acceptance rates.

Yet again, the main issue that traditional payment methods still struggle with is cross-border transfers. And for businesses moving money across borders, the delays and restrictions can be a huge blocker.

Does crypto payment rails increase conversion

Offering crypto payment rails allows businesses to reach a wider client base that is otherwise out of reach due to regulatory and currency conversion issues.

Payment becomes the least stressful part of the transaction instead of the most stressful. Crypto payment rails remove the biggest source of friction: delays.

Money arrives within minutes, not days, and it arrives exactly as intended, without hidden fees or intermediary deductions. Buyers feel more in control, and businesses can confirm payment instantly. That clarity reduces hesitation, speeds up decision-making, and often saves deals that would have died in the ambiguity of a pending wire.

Cross-border clients, in particular, convert at dramatically higher rates when offered a payment method that bypasses slow corridors, FX uncertainty, and overly intrusive bank checks.

Especially in private aviation industries where flyers want last-minute bookings.

Hugo from Altinium says, “Private aviation is about efficiency and time. Bank transfers can take up to 72 hours, while crypto offers instant, secure payments — which means flights can take off faster. With a new generation of clients already investing heavily in crypto, offering this option isn’t just convenient, it’s the future of seamless high-end travel.”

Read more: How private aviation company Altinium solved delayed settlements with crypto payment solutions

How high-ticket industries benefit from crypto payment rails

The highest-impact industries tend to share two characteristics:

transactions are time-sensitive, and values are high enough that delays cause real losses.

For time-sensitive industries such as real-estate, aviation, and automotive, crypto payments solve the biggest roadblock – delayed payments.

Cross-border real estate has grown consistently over the last decade, with real estate company Miami Realtors reporting 52% of new South Florida constructions were purchased by international buyers over the last two years.

The buyers operate in different time zones, manage assets across jurisdictions, and expect fast settlement to secure opportunities. In such cases, crypto payments enable faster, secure settlements.

Stablecoin payments arrive in minutes, regardless of time zone or day of the week. A buyer in Dubai can secure a property in Lisbon at midnight without waiting days for the payment to clear. Developers can plan better as they receive funds immediately without having to wait in uncertainty.

It also removes FX surprises as both sides know exactly what value is being transferred.This predictability smooths cross-border deals that would otherwise be delayed by volatile spreads or compliance bottlenecks.

As for the private aviation industry, data shows that short notice flights, often within 24 to 48 hours of departure are common, and a large majority of trips are booked within two weeks of the flight date. This means instant settlements are non-negotiable for aviation companies.

Crypto payment rails allow instant funds settlements so operators can focus on client needs and respond to short notice requests. All this without having to worry about FX conversion fees.

And it’s the same with automobile industries. When Mobile Autokeskus partnered with Swapin, they were responding to the client’s demands asking for Bitcoin payments.

And with that, they were able to offer their clients faster transactions, direct crypto payments in preferred digital assets, without any volatility risks.

A practical way for businesses to accept crypto payments

In most cases today, businesses don’t need to build the crypto payment solution from scratch. The simplest entry point is a crypto payment link, similar to a bank payment request but operating on crypto rails for efficiency.

A crypto payment link allows businesses to accept crypto payments from clients globally, without worrying about currency conversion fees and delays. And the best part, nothing changes for the finance team as they don’t need to manage manual reconciliations. Businesses receive the exact funds in the bank account in USD, EUR, or GBP.

A: No. All payments are automatically converted to EUR and transferred to your bank account, so your business never holds any crypto or needs a crypto wallet.

Q: Are there any additional costs for a business?

A: No, your client pays the crypto transaction fee. Swapin’s Payment Link is free integration and setup for you.

Q: Is it difficult to integrate into my existing payment systems?

A: Not at all. It is designed to integrate easily into your current payment process without requiring technical expertise. You just create a regular invoice for the customer and add a payment link with it.

Q: Is it safe for clients to use Swapin for large transactions?

A: Yes. Swapin is fully licensed, regulated, and audited, providing you with the same level of security and trust as traditional payment processors.

Stablecoin payments solution for cross-border transactions

Cross-border payments aren’t designed to meet the speed and scale necessary for modern businesses. It’s faster to launch a tech product than pay merchants across continents.

Unpredictable settlement, inconsistent fees, and operational friction compounds as businesses grow, and that’s become a normal state of affairs. Over the past five years, the supply and adoption of stablecoins have grown significantly, transforming the landscape of global business payments.

Stablecoin payments offer a way to move money without the delay and FX unreliability. It’s a single, programmable layer for global transactions that settles quickly, reduces FX complexity, and gives finance teams real-time visibility into cash flows. Common use cases for stablecoins in cross-border payments include contractor payouts, supplier payments, and marketplace settlements.

In this guide, we discuss how stablecoin payment solution work today, where friction comes from, and how businesses can reduce cross-border costs with stablecoins.

Global payments still rely on legacy networks built for an earlier era. Banks exchange messages, not money, across a patchwork of national clearing systems. Each country has different rules, different cut-off times, and different expectations for settlement. Regulatory frameworks and banking practices also differ significantly across regions, impacting the efficiency and reliability of cross-border payments.

The result is a system with a few recurring issues:

1. Slow settlement

Traditional bank transfers take 3-5 business days since settlement depends on correspondent banks and compliance reviews, none of which are visible to the sender.

2. High and variable fees

Cross-border payments typically include transfer fees, lifting charges, and intermediary bank fees – often discovered after the payment arrives.

3. Unpredictable workflows

Finance teams need to manage reconciliation and track payments manually, increasing operational overload and complicating cash management.

4. Fragmented rails

There’s no universal system for moving money globally. Every cross-border transaction is a bridge between two domestic systems with separate compliance and banking rules.

Businesses experience frictions in everyday workflows: contractor payouts, supplier payments, marketplace settlements, and refunds. These are high-volume, time-sensitive flows affecting the company’s ability to scale.

What stablecoin payments actually solve

Stablecoins simplify global payments by removing the need for intermediaries and reducing reliance on cross-border messaging networks. The system uses blockchain technology to enable fast, secure, and transparent transactions, allowing businesses to reduce cross-border costs with stablecoins.

Faster settlement

Moving stablecoins between two wallets settles in seconds. Because there are no correspondent banks, no business-day delays, and no regional cut-off times, the settlement is near-instant.

No central gatekeeper

As covered earlier, traditional payment systems are controlled by a handful of institutions that set fees, rules, and access. Blockchains don’t work that way as they’re open networks. Regulatory compliance is crucial in stablecoin transactions, and working with licensed providers helps ensure legal adherence in cross-border payments.

Reduced FX complexity

Using USD stablecoins takes FX out of the transaction itself. Stablecoins are typically pegged to fiat currencies like the USD or EUR, which helps maintain a stable value and reduces volatility. The customer converts to USD and the merchant receives it in USD or EUR directly into their bank account.

Reduced fees

On-chain transaction fees are considerably less, upfront and not dependent on international banking rules, making the process much faster and cost-effective.

24/7 availability

Blockchain networks operate continuously so global businesses can pay partners, vendors, or contractors at any time regardless of bank holidays.

Transparent by default

Public ledgers make it possible to trace funds and understand transaction flows end-to-end. Businesses can audit activity without waiting for statements from intermediaries.

Faster reconciliation

Every transfer has a unique transaction hash, giving finance teams immediate confirmation, real-time visibility, and simpler audit trails.

Protected by cryptography

Every transaction is secured with strong cryptographic methods, letting two parties transact directly without exposing sensitive details or depending on a middleman.

Industry adoption: who’s using cross-border stablecoin payments solution?

Cross-border stablecoin payments solution is rapidly being adopted by some of the world’s most innovative companies, transforming the way value moves in global finance.

Major players like Visa and PayPal have begun to leverage blockchain technology to facilitate international transactions, offering their customers faster, more reliable, and transparent payment options. For example, PayPal now enables users to send and receive stablecoins, making cross border payments more accessible and efficient.

Stablecoins such as USDC and USDT have become the preferred tokens for many businesses due to their ability to maintain a stable value, reducing the uncertainty often associated with other digital currencies. JPMorgan has taken a significant step by launching JPM Coin, a stablecoin designed specifically to enable instant cross-border payments for its institutional clients. Meanwhile, Circle, the company behind USDC, continues to offer compliant and transparent solutions for cross-border transactions, providing businesses with the confidence and flexibility they need to operate globally.

As more companies recognize the value of these solutions, industry adoption is expected to accelerate, making stablecoin payments a critical component of modern global finance.

How cross-border stablecoin payments solution flow work

Let’s say your international customer wants to make a purchase through your website, in such case, a typical cross-border stablecoin payments solution would look like this:

Step 1: The merchant generates a crypto payment link after signing up on a crypto payment gateway and sends it to the customer through invoice.

Step 2: Upon receiving the payment invoice, the customer clicks on the link directing them to the payment gateway.

Step 3: The customer then chooses to pay with their preferred cryptocurrency.

Step 4: The merchant receives the exact invoiced funds in EUR or USD directly into their bank account. Stablecoin solutions streamline merchant payments by enabling near-instant settlement and reducing transaction costs.

Step 5: After the funds are transferred, settlement is completed within a few minutes, depending on the network.

This method removes intermediaries and reduces waiting times, giving both sides more control over when to convert into their preferred currency.

Benefits of including cross-border stablecoin paymentssolution

1. Cost-effective cross-border transfers

As discussed previously, traditional cross-border payments jump through multiple banks, each taking a cut. Stablecoin transfers bypass most of that, allowing a direct route between sender and receiver.

When it comes to fees, credit cards sit in the 2–3% range, while stablecoin transfers range from anywhere between 0.5 – 1%. And while network fees vary, providers can charge processing fees from 0.3–2% and (0.5–2% for conversion fees).

Research suggests that stablecoin transfers are set to capture 12% of global cross-border transfer flows. Regulatory and interoperability development could enable stablecoins to move $1 in every $8 sent across borders by 2030.

2. Faster settlement means fewer cash-flow headaches

Cross-border transfers via networks like SWIFT can drag on for days, especially when emerging markets are involved. Meanwhile, finance teams spend hours managing manual reconciliation.

Blockchain rails settle within minutes. Compared to the 3 – 5 business days via SWIFT, stablecoins bring both the messaging and money-movement layers into one. What more, stablecoin settlements are final and irreversible, reducing chargeback fraud for businesses.

3. Simple and secure integration

Stablecoin payments solution don’t involve intermediaries, making the process safe and secure. And, businesses don’t need to build the payment solution from scratch to get started. While some financial institutions pursue internal development of proprietary stablecoin payment systems for greater customization and control, this approach requires significant technical and financial resources.

Stablecoin payment processors like Swapin take care of the regulatory and tech overhead, providing enterprise-grade solutions. So businesses can start accepting crypto and stablecoin payments within one day, without worrying about compliance or crypto management.

4. Reach a wider, global client-base

Over 700 million people own crypto globally in 2025. The number is only going to increase as regulations and tech developments improve across the board. Brands like Gucci, Starbucks, Tesla, and Ferrari have already started accepting crypto payments and a growing number of people want to pay with crypto for everyday transactions.

Unlike traditional financial networks that are controlled by central owners, blockchain-based payment systems operate without a central owner, making them more accessible and decentralized.

Read more: In 2025, merchants proactively opted for stablecoin payments at Swapin.

Traditional banking rails vs. stablecoin payments rails

Traditional correspondent banking systems have long been the backbone of cross-border payments, but they come with significant drawbacks: high costs, slow processing times, and limited real-time visibility. Each transaction often passes through multiple intermediaries, increasing the risk of errors and making it difficult for businesses to track the status of their funds.

In contrast, stablecoin rails leverage blockchain technology to offer a faster, more transparent, and cost-effective solution for cross border transactions. With stablecoin payments, companies can instantly send value across borders, with real-time visibility into every step of the process. For example, a business can use USDC to pay a supplier in euros, with the transaction settling instantly and at a fraction of the cost of traditional banking methods.

This flexibility and reliability make stablecoin rails an attractive option for companies looking to manage their cross-border payments more efficiently. By reducing the need for intermediaries and providing transparent, real-time access to transaction data, businesses stay in control of their capital, respond quickly to global opportunities, and reduce cross-border costs with stablecoins. As adoption grows, it’s clear that stablecoin rails are set to become the preferred solution for instant, secure, and cost-effective cross border transactions.

Get started with cross-border crypto transactions as a business

Cross-border payments shouldn’t slow down global businesses. Partnering with regulated payments providers make the process easier and faster. In the US, major banks like Bank of America and JPMorgan are leading the way in stablecoin adoption and expanding their use internationally, setting important trends for the industry.

Swapin is an EU-regulated crypto payments processor, offering businesses:

→ Built-in compliance

Businesses can avoid taking on licensing obligations. Swapin is EU-licensed, operating under the appropriate regulatory frameworks.

→ No crypto management

Swapin takes care of payment processing so accounting teams don’t have to manually reconcile and manage payments.

→ Zero integration and setup fees

Go live from day one and start accepting crypto from customers with zero integration and setup fees.

Crypto invoicing: how to accept crypto with zero integration

A crypto invoice is a digital invoice that allows customers to pay with crypto. It’s similar to a traditional invoice in that it includes date, amount due, description, invoice ID with an additional section for network and asset details for blockchain payments.

And unlike a bank or card transaction, a crypto invoice redirects customers to make payments to a dedicated wallet address or a hosted checkout page. Once the transaction is confirmed on-chain, the payment is final and there can be no reversals or chargebacks. Payments are settled within a few minutes since crypto transactions don’t include intermediaries, unlike banks.

Here are a few key features of a crypto invoice:

→ Option to pay with preferred cryptocurrencies as customers can choose their preferred cryptocurrencies to pay with such as BTC, ETH, or USDC

→ The amount due can be displayed in crypto or EUR/USD, depending on the merchant.

→ The merchant generates a unique wallet address for the invoice to which the customer makes the payment

→ Invoices in some cases can also include an expiration time within which the customer must complete the transaction

→ Most importantly, it includes details such as invoice number, issue date, due date, descriptions, and any other relevant info.

So although it’s similar to standard invoices, the rails underneath them are more efficient and cost-effective.

How crypto invoice solves complex issues with a single payment link

Businesses operating internationally rely on crypto invoicing because it resolves several recurring issues:

Faster settlement

Traditional SWIFT payments take 2–5 business days. Crypto payments on the other hand settle within minutes, thanks to zero intermediaries and banking restrictions.

Lower transaction costs

Cross-border transfers involve intermediary banks, adding up the fees. Crypto transfers take away the unnecessary steps so that the customer sends directly to the merchant, with minimal network fees.

Global accessibility

Regions that experience lack reliable banking infrastructure, especially for international payments, crypto provides consistent payment coverage without holding local bank accounts.

No chargebacks

Crypto payments are irreversible and final once confirmed, giving businesses predictable cash flow and reducing disputes.

More flexibility for customers

Customers can pay in their preferred cryptocurrencies or network, and merchants can receive in fiat (USD/EUR/GBP) directly into their business bank account.

Crypto invoicing removes much of the complexity and uncertainty associated with global billing.

How Crypto solution integrates with invoice management

Unlike traditional payment methods that rely on centralized banks, blockchain records each transaction on a decentralized ledger, making it nearly impossible to alter or counterfeit. Every payment is traceable and verifiable for businesses handling sensitive financial transactions.

Managing crypto invoices is straightforward and efficient and businesses can easily create, send, and track crypto invoices in multiple currencies, ensuring they stay organized and up-to-date with every transaction.

What more, solutions such as Swapin, don’t require merchants to hold or manage funds, reducing manual work and minimizing errors for the accounting team. With support for various cryptocurrencies and local fiat settlement, companies can cater to clients’ preferred payment methods while maintaining clear records for accounting and compliance.

Effective crypto invoice management not only streamlines the invoicing process but also helps businesses get paid faster and manage their cash flow with greater accuracy.

How to integrate crypto pay by link solution

Technically, Swapin’s crypto payment link solution for crypto invoicing requires zero integration. But here’s how to integrate crypto pay by link solution:

1. Invoice generation

The merchant creates an invoice that includes all necessary details about the product and/or service. This can be the amount due, due date, item details, payment address or hosted payment link, etc.

2. Customer makes the payment

Once the customer receives the invoice, they click on the link included that redirects them to a checkout page. Inside the payment gateway the customer selects the cryptocurrency they want to pay with and initiates the transaction.

3. Payment verification

The payment gateway verifies the payment details, checks validity, fund sufficiency, before finally authorising it.

4. Settlement and payout

After the payment is verified, funds are deducted from the payers account, and a notification sent confirming the payment.

5. Settlement

After the funds are transferred to the business’ bank account, the settlement can take anywhere between a few minutes to a few days, depending on the payment method.

Crypto invoicing fits into existing workflows while replacing slow, costly payment rails with faster alternatives.

How crypto invoice solutions simplify business transactions

Businesses catering to international clients can benefit from crypto invoice in a multitude of ways:

→ Faster settlement than wires. Crypto payments don’t go through the usual intermediaries that inevitably slow down processing and settlement time. Instead the payment is made directly between the customer and merchant, completing payment within 5 minutes.

→ Lower cross-border fees. Because of zero intermediaries, businesses save on transfer and conversion fees. This way, the merchant receives the exact invoiced amount in their bank account.

→ Broader global payment coverage. With lower exchange fees, businesses can now attract and reach a wider, international client base without worrying complex banking regulations and settlement times.

→ No chargebacks take away fraud concerns. For some merchants, crypto payments can be a new territory and an irreversible payment helps with dispute-related issues.

→ Easy to automate and reconcile so the finance and accounting team don’t have to manually reconcile. These automation and reconciliation features also simplify payroll management for businesses, making it easier to pay employees and contractors.

How to choose the right crypto invoice solution provider

Before deciding to accept crypto payments, it’s important for businesses to conduct a thorough research. Swapin is an EU-licensed and regulated crypto payments processor providing crypto payment link solutions. Businesses simply need to sign up on the platform, generate the unique payment link, and share it with crypto-friendly clients as they receive the settlement in fiat (EUR/USD/GBP).

With zero integration required, businesses can start accepting crypto within 1 business day.

“Because it removes the technical barrier. There’s no integration, no wallet setup, no custody, and no operational overhead required. Businesses simply generate the payment link, share it with their customers, and receive EUR/USD. That simplicity is why most clients start here.”

– Ivar Jaanus, Head of Business Development at Swapin

Interested in knowing more about how to integrate crypto pay by link? Learn more about how Swapin can help power your business transactions or get started today.

On-chain payments vs. traditional payments: what’s best for businesses

An on-chain payments system moves money directly between two digital wallets, with the entire transaction verified, recorded and settled on a blockchain network. It doesn’t include any third-party intermediaries and the blockchain itself is the payment network.

This takes out the core element of a traditional payment network that consists of multiple intermediaries, cutting straight to the settlement layer. For example, when you pay with a credit card, the payment goes through an acquiring bank, card payment network (Visa/Mastercard), and an issuing bank – further adding on to the cost and delay.

Compared to on-chain payments where the transfer, verification, and settlement all happen in one place, making the process near-instant.

Onchain payments follow a straightforward process:

→ First, the sender initiates a payment from their digital wallet. It’s similar to making payments from a bank account except the authorisation happens with a cryptic signature instead of a password.

→ Second, the transaction is recorded on a blockchain network, waiting for confirmation.

→ Third, after verification, it is added to a new block and validated under the network rules.

Finally, the settlement is completed almost instantly once it’s added to a block and the amount is transferred and cannot be reversed.

This takes away the 3-5 business days needed for traditional banks to process payments, ideal for cross-border businesses that often deal with fee hikes and delayed settlements.

The three core components of an on-chain payments process

Crypto on-chain payments consist of three core elements:

1. Digital wallets

This is the on-chain version of accounts, allowing users to send and receive crypto and digital payments. And typically consist of two types:

Custodial wallets where a third party site manages the keys and infrastructure, and thereby the funds.

And, non-custodial wallets where only the owner has full access to the keys, giving them full ownership and thereby the added responsibility of keeping the keys safe.

This is the settlement layer and each network comes with its own pros and cons in terms of speed, cost, and processing. The common blockchain networks include Ethereum, Solana, Polygon, and layer 2 networks.

The blockchain network handles the transaction, validation, and finality.

3. Smart contracts

This is an automation layer to crypto on-chain payments, embedding business rules into the transaction flow. So instead of manual revenue splits, escrow services, reimbursements, subscription billing, or multi-party settlements, smart contracts execute those steps automatically as part of the payment itself.

How traditional rails actually work

Traditional payment rails are the underlying banking networks and financial institutions. They weren’t designed as a unified system, rather they were built to solve specific problems throughout several years.

It’s why today’s payment landscape is fragmented with each having its own processing and settlement times.

What are different types of traditional payment rails

1. ACH or Automated Clearing House

ACH is the US system for low-cost, bank-to-bank transfers, processing payments in batches meaning settlement typically takes a full business day or longer. It’s common for payroll, direct debit, and recurring billing. However it’s domestic, slow, and not designed for real-time transactions.

2. SWIFT

SWIFT is a global messaging network banks use to move money. The money moves through a chain of correspondent banks, each with their own fees and processing speed. Time zones, compliance checks, and manual review makes it a slow, time-consuming process.

3. Wire transfers

Wire transfers are sent individually and are faster. The downside is they come with high fees and strict cutoff times.

4. Card networks

While card payments are instant for consumers because authorization takes a couple of seconds. Merchant settlements take much longer and include interchange fees, chargebacks, and a complex mix of acquirers, issuers, and processors in the middle.

5. RTP or Real-Time Payments

RTP systems aim to modernise bank transfers with near-instant settlement. They’re technically strong, but adoption is still maturing. Many banks haven’t integrated them fully, and usage varies widely across regions and institutions.

What slows down traditional payments

Most systems batch, queue, schedule, or pause transactions at some stage, making the settlement process longer, especially for cross-border payments.

KYC, AML, fraud checks, and dispute handlings are done by each banking network and institution and the process only becomes more complex with international payments.

SWIFT relies on correspondent banks that charge arbitrary fees. This adds cost, delay, risk checks and operational overheads.

How are crypto on-chain payments different

When businesses compare on-chain payments to traditional rails, speed or fees are generally the most talked about reasons. However, the actual impact involves accounting, treasury, compliance, and support teams managing the day-to-day realities of moving money.

Faster settlement speed

Traditional rails split a payment into stages: authorisation, clearing, and settlement. And for each institution involved (bank, processor, issuer, etc.), updates its own ledger independently.

A card payments authorise in seconds, but the merchant only receives funds days later because settlement happens on a fixed cycle. SWIFT transfers rely on time zone alignment and compliance reviews that can delay transfers well beyond what customers expect.

Crypto on-chain payments reduce these stages so validation and settlement occur together.

Once a transaction is confirmed on-chain, it is final and irreversible. So not only are payments faster, it changes how teams manage payouts, liquidity and cash flow. Instead of planning around batch windows, cutoff times, and pending states, companies operate on a real-time ledger.

Cost-effective and accessible

Traditional fees include interchange, processor fees, wire fees, correspondent bank deductions, FX spreads, and chargeback exposure. Making the total costs unpredictable.

On-chain fees behave differently. It’s transparent, determined by network demand, and typically separate from the transaction amount, making it more economical for high-value payments or high-volume payouts.

The real winner is the operational cost reduction. When settlement, reconciliation, and record-keeping converge into one system, businesses eliminate layers of internal processing work that would normally require manual review, dispute handling, or multi-system matching.

No more manual reconciliation

Traditional rails require businesses to reconcile across multiple ledgers with each system logging transactions differently and often on different timelines. Finance teams spend a considerable time on manual reconciliation investigating mismatches, failed transactions, partial settlements, and ambiguous status codes.

On-chain payments remove this multi-ledger complexity.

Businesses don’t have to request settlement files or wait for the acquiring bank to update records. This reduces reconciliation work for the teams, resulting in fewer overheads, support escalations, and accounting adjustments.

Smoother and faster cross-border operations

Traditional international payments depend on correspondent banking networks, currency liquidity, and jurisdiction-specific compliance checks. Transfers vary depending on the region as some countries could take days and arrive short of the expected amount due to intermediary fees.

For crypto on-chain payments, a transfer to Singapore works the same way as a transfer to São Paulo. Plus, stablecoins payments eliminate most FX-related friction by allowing international value transfer in a unified digital currency and only converting to local currency when needed.

Read more:How stablecoin payments help businesses with cross-border money movement.

Security fares better

Traditional rails rely on institutional security where accounts are password-backed, fraud detection is centralised, and reversals act as a corrective mechanism.

On-chain payments rely on cryptographic security and key management, where control is absolute and reversals aren’t part of the design. This reduces fraud vectors like chargeback abuse and account takeover but increases the importance of custodial controls, multi-sig wallet setups, and internal access policies.

Taken together, these differences reshape the daily operations of any company that moves money at scale. On-chain payments consolidate the entire lifecycle of a transaction into a single, shared, final ledger, making the financial workflows cleaner.

And while traditional rails remain essential for credit, consumer protections, and regulated flows, from an operational standpoint, the contrast is evident.

Businesses can now accept crypto payments without worrying about development costs and regulatory compliance. Crypto payment gateways offer two simple ways businesses can accept crypto payments.

Option 1: API integration

A crypto payment API is well suited for businesses needing more customised solutions. With this, businesses can automate transactions, integrate wallets, reconcile at scale, or create an embedded payment checkout solution into their website.

The API solution massively reduces time and workload as businesses don’t need to build the payment infrastructure from scratch or worry about regulatory compliance.

Option 2: Payment link

The crypto payment link solution doesn’t require any integration. Businesses simply need to generate a payment link, share the link along with the customer invoice, and enable customers to pay with their preferred cryptocurrencies while they receive the exact invoiced amount in EUR, USD, or GBP.

Compared to the API solution, it’s faster and requires absolutely zero integration, making it a low effort payment method for businesses that are new to crypto payments but still want to offer it to clients.

Making cross-border payments efficient with crypto on-chain payments

Accepting crypto payments is now just as simple and quick, especially for cross-border businesses. Swapin is a regulated crypto payment processor enabling businesses to start accepting payments within one business day without any integration or setup fees.

Ready to scale your business? Reach out to us or get started today.

Stablecoins go mainstream: why merchants are opting for crypto payment in 2026

As we gear up for 2026, it’s time to reflect on how the crypto payments industry fared this year.

And to get a clearer picture on the industry shifts that are playing out, we sat down with Ivar Jaanus, Swapin’s Head of Business Development. Working directly with high-value merchants, understands user behaviour, adoption dynamics, and industry trends on the ground level.

The three insights that set the tone for 2025, are:

1. Stablecoins have become the default cryptocurrency options as merchants proactively offer it to clients alongside traditional payment methods.

2. Volatility, compliance, and operational concerns are no longer deal-breakers. Merchants are increasingly partnering with trusted providers that manage regulatory and operational requirements.

3. Clients now want to pay with crypto and that’s a major factor driving merchant adoption. Signalling that genuine demand will inevitably win.

Q:What are the top 3 changes you noted in client behaviours in 2025?

Ivar: High-value clients are no longer exploring crypto payments, they’re directly requesting for stablecoin payment options. And, speed is a non-negotiable. It’s safe to say that crypto payments is moving from an alternative method to a mainstream, preferred option.

This is notable especially in high-ticket, time-sensitive industries such as private aviation that cater to international clients.

Qur partner client, Nathan Davis from Finer Aviation mentions in an earlier interview how ‘moving large amounts of money at very short notice’ is incredibly common and businesses don’t want to wait days for payment settlement.

In such cases, crypto payments work as an instant settlement solution, especially for cross-border clients ready to pay with their digital assets.

Q: Were there any specific countries, regions, or industries that saw a high demand growth in 2025?

Ivar: Luxury sector across Southern Europe, particularly Spain, France, Italy, Malta, and Cyprus saw the strongest demand. Comparatively, Northern Europe remains more conservative and cautious in their approach to adopting crypto payment methods.

And In terms of industries, private aviation, yachting, watches, and supercars were the strongest verticals.

In a 2025 survey, 60% of buyers now make direct crypto payments online and 15% of those are high-net worth individuals who use it for luxury purchases. And with the luxury market projected to exceed $500 billion by 2029, crypto use cases are evolving beyond investment and trading, thanks to crypto payment providers.

Q: Are you sensing a shift in how businesses approach crypto payments? Is it primarily to catch up with the competition, meet client demands, or position themselves as a forward-thinking company?

Ivar: I’d say it’s a mix. That being said, client demand is the strongest driver for adoption. Followed by competition since companies don’t want to fall behind. And being seen as the forward thinking brand is an added benefit that comes with it.

When you’re keeping up with the evolving client demands, you’re automatically a customer-centric, forward-thinking brand.

And this explains why zero-integration crypto payment solutions are becoming popular amongst businesses looking to accept crypto without having to build the infrastructure in-house.

Q: What payment solutions/use cases saw the most growth this year? What do you think is driving the growth?

Ivar: Definitely the SwapinCollect crypto payment link solution. It’s because the product requires no integration or crypto management and works as a great starting point for businesses accepting crypto payments for the first time.

When you take away the regulatory compliance, technical integration, and risk management hassle, businesses are more receptive and likely to adopt newer payment methods.

Misconceptions and concerns cleared out

Q: What are the common misconceptions businesses have about crypto payments, and do we, as Swapin, handle them?

Ivar: Two misconceptions I hear on the regular.

One, crypto payments are “complex” and require running wallets or taking volatility risk. Swapin removes all of that. Merchants never touch crypto. They simply receive EUR/USD to their bank account.

Two, people automatically think of BTC and ETH when you mention crypto payments, when in reality, Stablecoins are more commonly used for payments. As for the merchant, it really doesn`t matter which currency is used, they receive in fiat.

Between January 2023 and February 2025, businesses processed over $94 billion in stablecoin payments. And at Swapin, stablecoins is the most commonly processed cryptocurrency as well.

Swapin stablecoins vs other cryptocurrencies breakdown

Q: What concerns keep businesses from accepting crypto payments? What was the deciding factor for businesses to move to the commitment stage?

Ivar: The main concerns I hear from clients are about compliance, volatility, and operational risk. Once that’s taken care of for them, they’re not hesitant and are rather eager to come onboard.

Q: How have the recent regulatory updates affected how businesses view/manage crypto payments? Did regulatory clarity help close deals better and faster?

Ivar: Most merchants aren’t too deeply familiar with crypto-related regulations, they focus on their core business. It’s like, if you buy a car, you don`t need to know how the engine works; you just want it to drive. It’s the same when it comes to payment providers. The merchants want payment partners they can trust to take care of everything “under the hood”, so that everything just works how it’s supposed to work.

Q: Why is the crypto payment link the easiest starting point for companies accepting crypto for the first time?

Ivar: Because it removes the technical barrier. There’s no integration, no wallet setup, no custody, and no operational overhead required. Businesses simply generate the payment link, share it with their customers, and receive EUR/USD. That simplicity is why most clients start here.

Q: How do you see stablecoins performing in 2026 compared to in 2025, especially since the regulatory developments and institutional adoptions.

Ivar: All current predictions point toward strong growth in stablecoin usage and the momentum from 2025 is expected to accelerate further. With clearer regulation and wider institutional adoption, 2026 will be the year of stablecoins.

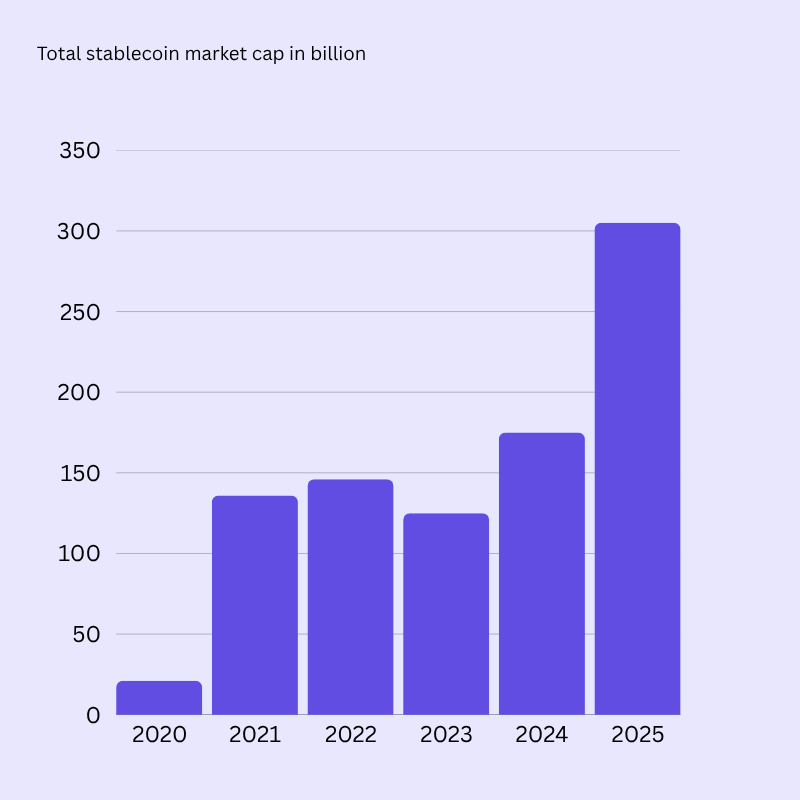

Currently, stablecoins total market cap is at $302 billion, and it’s only projected to grow. In fact, Citi Group predicts stablecoins base case estimate issuance to reach $1.9 trillion and $4.0 trillion in bull case by 2030.

Stablecoins market cap as of Nov 2025

Q: What trends and developments are you looking forward to in 2026?

Ivar: More companies are moving from treating crypto as a one-off exception to making it a normal part of their payment stack.

Instead of waiting for a client to specifically ask to pay in stablecoins, they are proactively offering it alongside traditional methods. It is becoming a built-in option, similar to card payments or bank transfers, because it helps them close deals faster, reach international clients more easily, and remove friction from high-value transactions.

Looking ahead: What to expect in 2026 for crypto payments

2025 marked a clear turning point that crypto payments are not a niche product for niche audiences.

Institutional adoption, regulatory clarity, and merchant adoption all point towards stablecoins becoming the norm. And in this case, simplicity wins. Businesses are looking for zero-integration, instant settlement options that don’t burden them with infrastructural responsibilities.

Learn more about how Swapin can help power your business transactions or get started today.

Shaping the global luxury business landscape: Interview with Alexander Chetchikov

Earlier in October 2025, Swapin became a proud member of the World Luxury Chamber of Commerce (WLCC), a global network for leading luxury brands.

The WLCC provides its members a platform with exclusive access to elite networking opportunities, allowing businesses to scale and reach a wider luxury market.

The WLCC is built on the legacy of the Luxury Lifestyle Awards, with 16 years of honoring global luxury brands, boasting a network of over 5,000 luxury businesses across 100 countries.

We had the pleasure of interviewing the President of WLCC, Alexander Chetchikov, to discuss how the luxury business sector is at the forefront embracing innovation and expansion, evolving customer expectations, and predictions for the 2026 luxury business sector.

Q: Alexander, in your own words, please describe the World Luxury Chamber of Commerce’s vision and mission, and its role in shaping the global luxury business landscape.

Alexander: Our vision is to become the largest global network for professionals working in the luxury sector. The primary goal is to unite the numerous, often fragmented segments of the global luxury market, acting as a catalyst for growth and deeper professional collaboration.

The Chamber provides brands with a strong platform for partnership and the exchange of valuable expertise. In this role, the WLCC shapes the global luxury landscape by creating a unified voice and shared standards for the entire industry.

To this end, the Chamber organizes and supports initiatives such as World Luxury Day and the Luxury Lifestyle Awards, which recognize and celebrate talent across the sector. Additionally, the WLCC conducts educational programs aimed at enhancing professionalism and knowledge, as well as hosting networking events that promote cross-border collaboration and meaningful exchange.

Q: Luxury has always been built on heritage, craftsmanship, and exclusivity. How do brands maintain these traditions while embracing innovation and technology?

Alexander: To preserve their essence, luxury brands today must skillfully balance age-old traditions with rapid technological change. They do not abandon their roots – a heritage, craftsmanship, and exclusivity – but rather use technology as a tool to amplify and showcase them.

This is evident in how digital platforms and AR/VR technologies create immersive stories about a Maison’s past, making its heritage accessible to new generations. In craftsmanship, innovations such as 3D printing or advanced materials expand creative possibilities, but the most valuable finishing touches always remain handcrafted.

Exclusivity is also evolving: it is now defined not only by rarity but by personalization – enabled by data – or by digital authenticity through blockchain and NFT technologies. These elements allow brands to remain desirable and relevant in an ever-changing global landscape.

Rising consumer expectations

Q: Consumer expectations are evolving. Convenience, speed, and digital experience are now cornerstones of luxury business. How are high-end brands adapting to this shift?

Alexander: Modern luxury brands understand that convenience, speed, and digital excellence are now integral to the luxury experience. They create omnichannel ecosystems that seamlessly merge online and offline interaction – introducing express delivery services, AR fitting rooms, and AI-powered instant support – ensuring that every touchpoint reflects the same level of refinement.

Q: How do you see instant payments improving exclusivity and premium service for customers expecting smooth, simplified solutions?

Alexander: Instant payments elevate the purchasing process, turning it into part of the impeccable luxury service experience.

Payment trends in the luxury sector

Q: Are payment expectations – speed, flexibility, and currency options – higher in the luxury business segment compared to other industries?

Alexander: Absolutely. Expectations around payments are significantly higher in the luxury sector. Clients purchasing premium goods expect the transaction process to match the quality of the product and service itself: instant speed, maximum flexibility (from traditional cards to cryptocurrencies), and freedom to choose the payment currency without friction.

Any malfunction, delay, or inconvenience disrupts the exclusive experience, undermines brand perception, and diminishes value in the eyes of clients who expect flawlessness in every detail.

Q: How do modern payment methods simplify cross-border and high-value transactions for international clientele?

Alexander: While I am not a payments specialist, from discussions with colleagues it’s clear that modern payment solutions are essential for simplifying cross-border and high-value transactions in the luxury market.

They bypass traditional banking complexities – reducing fees and delays – and digital wallets or blockchain solutions provide security, instant settlement, and transparency in currency operations. This aligns perfectly with the expectations of clients making significant international purchases.

Luxury market predictions for 2026

Q: What trends have you noticed in the luxury business industry in 2025, and which do you predict will accelerate in 2026?

Alexander: I don’t think 2026 will be radically different from 2025, but several trends are clearly gaining momentum:

Hyper-personalization through predictive AI that anticipates future client needs.

A complete merger of “phygital” retail, where physical and virtual experiences become seamless.

The circular economy – resale and rental – becoming both a norm and a new status symbol.

Growth of immersive, educational luxury experiences focused on learning and self-development.

Increasing use of Web3 technologies for authentication and secure ownership records.

Crypto payments fit right into the luxury sector

Q: Crypto payment solutions have come a long way. How do they fit within the luxury business sector?

Alexander: From my perspective, crypto payment solutions integrate naturally into the luxury space because they combine instant settlement, confidentiality, and security – qualities essential for high-value purchases.